|

|

Russian market of mobile terminals in the 4Q 2005

Press release,

February

13-th 2006

Statistics. The official sales of terminals on the Russian market reached 9330 thousands of units*, in the 3Q the amount of shipments was 8738 thousands of terminals. The growth was 6.7 percent, which is not typical for this season. The amount of grey market in the fourth quarter had decreased to 1.7 percent, this was caused by problems at the Russian customs, and overall growth of official sales. The term “grey market” in current situation should only mean smuggled products, which is delivered without passing through any official “channel”. The average price for models in the 3Q became 102.6 Euros. The growth of replacement market by the end of the quarter was 72%. The total amount of the market in 2005 became 33 million 280 thousand of terminals.

* Sell-in data of the manufacturers are used here and further

Short description of the situation. The main events of the mobile phone market in the 4-th quarter were the following:

- The situation at the customs, lack of guaranteed mobile phone shipment channels for the Russian market ;

- The growth of replacement market, saturation of regional markets due to expansion of federal brands;

- Hanges in user's preferences, as a result – drop in sales during pre-New Year season.;

Russian customs

In august of 2005 department “K” from MIA of Russia made several raids not only to customs terminals, but outside them, this lead to impressments of significant mobile phone supplies. This phones were sold during the 4 th quarter of 2005 at regional markets through 1-day companies, no court verdicts that would confirm such realization were made.

MIA of Russia started affecting not only the distributors of mobile terminals, but also the national customs committee. As a result of such pressure one's seen demonstrative growth in tax collection from mobile phone import, Russian residents have heard about it during the 4-th quarter from the customs service. Like we've already told you, these kind of actions were done only in demonstrative purposes, and had only negative affect on the market. The customs committee neutralized all schemes of semi-legal delivery of goods through Moscow terminals. Most methods were based on lowering the actual price of shipment. Meanwhile same kind of channels continued to operate in St Petersburg , which lead to redistribution of shipments through this city. By the start of 4-th quarter Moscow companies had to pay for delivery and custom clearance of one unit around 26-29 percent (23% is the official tax) of the whole phone's price. Meanwhile distributors from St Petersburg had to pay only 12-14 percent with delivery included. After gaining advantage due to government's actions distributors who are based in this city increased their activity by 2-3 times.

The current situation was inappropriate for Moscow companies and they decided to address phone manufacturer's representatives, demanding in ultimate way limitation of shipments to Russia, making it available only for official distributors. This allowed avoiding the existence of current semi-legal schemes of shipments with participation from one-day companies, and stopped sales of terminals outside Russia. Manufacturers organized common position only by the end of the year and agreed to Moscow 's distributors demands. Companies from St Petersburg agreed as well, formally. But these agreements did not become pledge of transparent market foundation, since the market still has intermediate companies that provide import of products with lowered customs rate (12-15% for customs clearance).

Customs actions did not affect the companies who are importing terminals to Russia unofficial, without interacting the representatives of mobile phone manufacturers and established channels. Basically companies that are concentrated on smuggling were not affected. At the same time all big distributors were under fire, since different conditions for different towns disallowed having same price level of one and the same products. The situation got even worse with Ukraine that had no control of the import, models that were supposed to go for sale in this country had the same marking as for Russian market and the same software sa well. Several small companies with turnover of less than 50 000 terminals per quarter decided to buy equipment in Ukraine and ship it to Russia. The difference in retail price between two markets starts from 15%, and in case you start digging from wholesale prices, the difference between Ukrainian wholesalers and Russian retailers can be up to 30-35% for certain positions. From the 4-th quarter we can see an explosive growth of consumption of mobile terminals in Ukrainian market, it is not cased by new mobile phone users, it's the orders from Russian companies. During the 4-th quarter Russian customs had no cases of mobile phone shipments arrests that come from Ukraine to Russia. This caused negative expectations by distributors, and affected sales in wholesale channels. Regional players preferred buying small portion of phones from Ukraine that would cost less than paying for completely “white” phones from Russian companies. In the first quarter of 2006 shipments from Ukraine will affect the Russian market the most.

Regional companies with closure of delivery channels of terminals for their partners from Moscow, problems with shipments in the background decided to look for their own ways to buy equipment. The demand in big cities had overcome the supply greatly. Companies had no experience in mobile terminals decided to work on possible channels of their shipping. Yekaterinburg became one of these channels, mobile phones from China are shipped here. The channel became completely smuggled, since the models are not supposed to be sold in Russian market, they don't have the required software or the package. But price of such phones is low, and it is reasonable to print out additional manuals in Russian and perform firmware updates. The capacity of this channel is from 20 K terminals monthly. This is not the only exception, in other big cities there are various channels of equipments delivery.

Big distributors had to compete not only against themselves, but also the grey market. This lead to impossibility of retail price reduction for mobile phones, let's remind the fact that after August's events the price went up by 25-30 percent. Maintenance of high margin for mobile phones for big retail networks becomes the only way to survive in the current situation of the unstable market. The companies are trying to compensate their losses in August and September by high prices, as well as an attempt to create operative stock for today. But on the other hand these prices formed a black market, they activate unofficial shipments and blur sales share of "white" products.

In order to normalize the maintenance of one and the same working conditions for all distributors, actions from customs and also from the manufacturers are required. Due to heterogeneity of interests in customs committee, big competition among the manufacturers one can't expect the settlement any time soon. The factor of instability will remain actual at least until the end of summer. Starting from the 1 st quarter of 2006 the share of teh "grey" market will grow, but it will be hard to differ models targeted for Russia and those imported for Ukraine .

The current situation is a great menace to franchise projects, mostly for Divizion and Cifrograd. In conditions of overpriced phones from the holders of franchise their partners will start losing the market share and will be unable to fulfill the obligations that are stated in the contracts. Fight for market share and as result buying equipment not from the holders of the brandname, but other sources will become logical action for them. This will hit sales of Divizion, Cifrograd (Severen in this case), decrease them and also form negative image of these brandnames in the eyes of the customers (low quality service, phones that are not supposed to be sold in Russia , lack of warranty, etc). For companies holders of franchise it's impossible to control the process of mobile phone realization, they will not work on illegal schemes of shipments, this doesn't look highly realistic. They are losing the competition due to price. The decrease of sales share by ordinary distributors, not those who are using franchise can be also noticed, but it's different in speed.

Replacement market, regional markets

Russian market of mobile terminals is moving steadily to the stage of saturation, we can see that by the decrease in interest to budget models of middle segment (not the cheapest solutions, but middle ones in the range of 65 to 110 USD), we can notice the growth of replacement market. In 2004 the replacement market became only 48%, meanwhile in 2005 this market had 78% of total sales amount. The maximal size of this market is 86%, it will be reached in the 2-nd quarter of 2006 or slightly afterwards. The supply demand on more expensive models, appearance of consumers class that have definite and deliberate needs created the demand in the 4 th quarter of 2005. The choice of the phone for the customer becomes more deliberate, the following parameters are dominating in his wishlist:

- Design, outlook's attractiveness, it should match person's presentation about himself

- Brandname, its image and prestige

- Phone's price

- Good display, polyphonic ring tones

- Certain functionality

- Other features

The research of changes in customer's behavior was made in September and October 2005 in 9 big cities, overall selection reached the amount of 2675 people. Same kind of research made a year ago (only Moscow, selection of 350 people) showed that the consumers relate mainly to the technical components of the phone, this means the display and polyphonic ring tones, only after this the consumer was interested in the price and brandname. Direct comparison of these results is impossible, but you can get quite the picture of the market's evolution. Nowadays the customer looks on the design, additional features are not that important. The success of Motorola RAZR V3 clearly demonstrates such changes in customer's behavior. Loyalty to one or other brand starts playing a big role in choosing the phone. The growth of Nokia phones consumption in retail networks is caused by the same changes that we had described above.

Lack of boost in sales in the pre-New Year period is cased by changed behavior of consumers, as well as the fact that the phone is no longer part of the status role for certain kind of consumers. In Russia the market of expensive phones had already formed, its size is maximal for European markets. At the same time a lot of consumers don't see status constituent in a mobile phone, it's a simple object of everyday life. The market of exclusive models in Russia overcomes the one in Italy by 5.5 times minimum. Unofficial sales of Vertu phones overcome official ones, for Russian consumer this product became massive in certain circles, even though the manufacturer is positioning it as unique offer with limited sales.

Starting from the 2-nd half of 2005 we also start watching at the foundation of loyal customers class in relation to retail networks. Before the price of the phone was a decisive factor for customers when they had to choose which place to buy their phone at, now they are taking the company's reputation, service quality and additional services into consideration. With usage of additional services the convenience of attending the salon, its location and availability become a top priority. This allows Euroset to form a high collection of payments for operator's services, and that's not all. Sales of accessories get a boost as well, from the very same type of customers. This means that besides loyalty to retail network, its brand, the amount of shops, their location in the settlements, covering density affect the success.

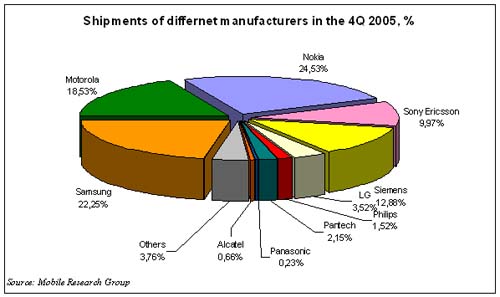

In the situation with Russian customs regional players receive additional chances in competition with federal networks. Different price offers on many positions exist, this allows formation of more-less balanced offer. But negative tendencies are still strong, a lot of companies become franchisers, a lot of companies prefer selling their business, quitting it with minimal losses. Results of the 4-th quarter of 2005

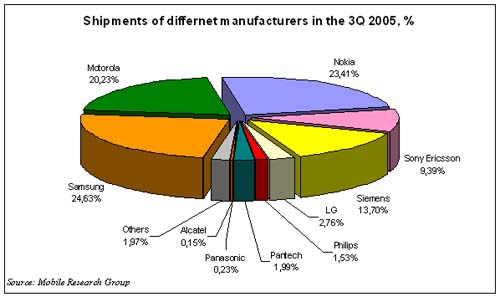

In order to understand the situation you have to look at the situation during 3 rd quarter of 2005. The manufacturers had the following market shares.:

In the fourth quarter Nokia continued intensifying of its presence on the market and managed to take the lead, this became possible with the help of Euroset's position. During the 4-th quarter this retail network gave directions to sell Nokia's equipment in prejudice of other manufacturers, this strategy is still active. By the end of the year Nokia is still on the 2-nd place, this is caused by bad control over terminal shipments. One of the big distributors is systematically laying in stock, but it doesn't ship them in full scale at the Russian market because it lacks retail partners nor its own network. The phones get sold in Eastern Europe and even African countries. We do not take these phones into consideration, even though they are accounted by Nokia as the ones shipped to Russian market. The phones don't get shipped here physically, therefore they should not be accounted. Short-term prediction for Nokia is positive, the only competitor here is Samsung, but its model line-up is more poor, there are no massive products for smartphone line-up will prevent Korean company from making big impact on Nokia. Strict control over the distributors, shipments, big activity in ATL and BTL channels is positive side of Samsung. These companies will be competing in order to become the leader in 2006, so far Nokia looks like the favorite in this melee.

Motorola was unable to form its model line-up and all sales were based on several key models, including Motorola RAZR V3. This model is an absolute bestseller in its class, and its sales can be compared with ones in the low-end segment. The manufacturer is increasing the proposal for this model by case color variations. The model has big life cycle and will be seen in retail sale up to the autumn of 2007.

Besides RAZR budget solutions from Motorola had pretty good sales, main factor was the phone's price. The company started feeling impact from Siemens and Nokia in this segment. High sales are also typical for Sony Ericsson's budget solutions.

In future we should expect Motorola to become third, there won't be any boost in retail market's share for American company. Siemens is not a menace to Motorola, although by decreasing price for budget phones German manufacturer managed to increase its market share and acquired 4 th place. The change of name to BenQ, appearance of the second word on the phones will affect negatively on customer's perception. At the same time whole different in terms of design and ideology phones might refresh the situation.

Siemens starts feeling pressure from Sony Ericsson, we should expect German company to substitute places with Swedish-Japanese tandem in the end of the 2-nd beginning of the 3-rd quarter of 2006.

Sony Ericsson fixed its sales, there are new models ready to be released, the company has good status in the middle and high priced segments. The negative side for the company is the lack of big line-up, even though the popularity of the brand is increasing constantly. The negative factor is a growth of grey shipments mostly from Ukraine .

LG has occupied the 6 th place and the company looks kind of confident on that one. Rotation and constant updates of the model line-up help to achieve this result. LG's main partner is Euroset, and the company decided that they can interrupt their relationships with another big retail player - Svyaznoy. This means that from now on LG will be focused only on the one big player. As long as Euroset needs substitutes of Samsung's phones LG's and Pantech's sales will be secured, but they will decrease in future since the manufacturers do not have formed market sales.

In fourth quarter we've seen rapid loss in sales for companies from the 2-nd echelon, a lot of distributors decided to break-up with these manufacturers. In future we will only see worsening of this situation for Fly, a set of big retail players decided to stop cooperation with this manufacturers (with exclusive distributor Meridian Telecom to be precise). Panasonic is leaving the GSM market, it will not manufacture them anymore. Alcatel did not have sales during the last 6 months, and this negatively affected its position (in the 4 th quarter we've conducted neglected before numbers of sales for this company). Sharp had disappeared from the market completely, same fate is expected for NEC, it does not have a new model line-up of 2006. Sales of i-mode phones for MTS are not large. The stable position is kept by such companies as Philips and Voxtel. Sagem managed to make a leap forward for the first time, and shipped 245 thousand of terminals during this quarter.

Results of 2005, predictions for 2006

The growth of market in 2005 had continued, but the temps had slowed down with the ending of regional expansion by the operators. In 2006 the market will continue its growth, but this year will become the last for growth of the market. MRG estimates up to 38-39 million of terminals might be shipped during 2006. The changes in demand structure operates the growth of average price for the terminal, this tendency will remain actual for 2006.

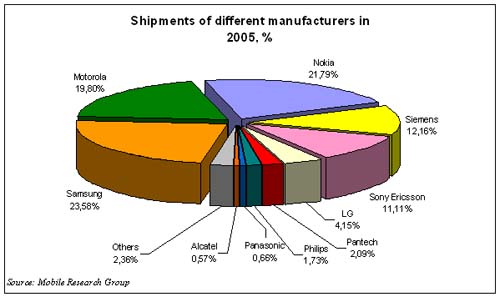

The company's shares in 2005 looked the following way:

About Mobile Research Group

The main activity of Mobile Research Group (http://www.mobile-analytics.ru) - is mobile terminals market researches in Russia. The company analyses the competitive situation of all mobile phones manufacturers available on the Russian market, and researches retail and wholesales of mobile terminals. Basing on analyzed statistic data the company makes a forecast of the mobile terminals market development for some period (up to one year). According to concluded partnership agreement once a quarter the company presents a market analysis report, where the most considerable events and their results are marked.

Publishing data contained in this press release

without a link to the Mobile Research Group as a source of

information is prohibited. We reserve the right to change

data published above if any new circumstances or new information

earlier unknown to us arise.

© Mobile Research Group, 2005

© Mobile Research Group, 2006 Eldar Murtazin (eldar@mobile-review.com)

Translated by Alexander "Lexx" Zavoloka (alexander.zavoloka@mobile-review.com)

Published - 20 February 2006

Have something to add?! Write us... eldar@mobile-review.com

|

News:

[ 31-07 16:21 ]Sir Jony Ive: Apple Isn't In It For The Money

[ 31-07 13:34 ]Video: Nokia Designer Interviews

[ 31-07 13:10 ]RIM To Layoff 3,000 More Employees

[ 30-07 20:59 ]Video: iPhone 5 Housing Shown Off

[ 30-07 19:12 ]Android Fortunes Decline In U.S.

[ 25-07 16:18 ]Why Apple Is Suing Samsung?

[ 25-07 15:53 ]A Few Choice Quotes About Apple ... By Samsung

[ 23-07 20:25 ]Russian iOS Hacker Calls It A Day

[ 23-07 17:40 ]Video: It's Still Not Out, But Galaxy Note 10.1 Gets An Ad

[ 19-07 19:10 ]Another Loss For Nokia: $1 Billion Down In Q2

[ 19-07 17:22 ]British Judge Orders Apple To Run Ads Saying Samsung Did Not Copy Them

[ 19-07 16:57 ]iPhone 5 To Feature Nano-SIM Cards

[ 18-07 14:20 ]What The iPad Could Have Looked Like ...

[ 18-07 13:25 ]App Store Hack Is Still Going Strong Despite Apple's Best Efforts

[ 13-07 12:34 ]Infographic: The (Hypothetical) Sale Of RIM

[ 13-07 11:10 ]Video: iPhone Hacker Makes In-App Purchases Free

[ 12-07 19:50 ]iPhone 5 Images Leak Again

[ 12-07 17:51 ]Android Takes 50%+ Of U.S. And Europe

[ 11-07 16:02 ]Apple Involved In 60% Of Patent Suits

[ 11-07 13:14 ]Video: Kindle Fire Gets A Jelly Bean

Subscribe

|