Russian market of mobile terminals in the 2Q 2004

Press release, July 22 2004

Statistics. Official shipments of GSM-terminals

on the Russian market suggested 4 949 thousand terminals

(heere and after the sell-in figures of the companies are used,

not retail sales), while in the first quarter officials shipments

suggested 5 107 thousand terminals. The decrease of sales was 3

percent, which happened due to the April glutting after

the stabilization of the customhouse work. The grey market shipments

suggested 4 percent, which is very low of for the

Russian market, it may be compared to the results of the previous

quarter (5 percent). The sales scale changed for the main five manufacturers

as well as their positioning on the market. The value of shipments

suggested 523 million 572 thousand Euros.

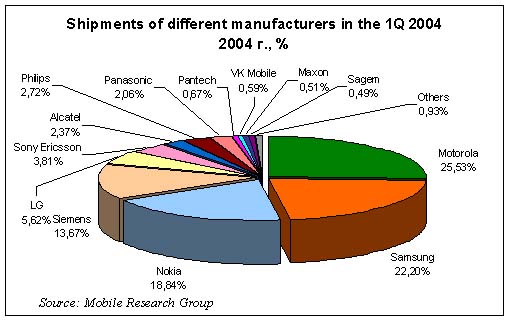

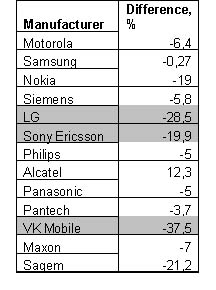

Sony Ericsson took the fifth place for the supplies of unit shipments

having overridden LG. The average price for Nokia became less than

100 Euros. The decrease of average price was typical for all the

manufacturers with Samsung and Alcatel being exceptions.

The forecast of the market for 2004 remained the same; official

shipments of GSM-terminals will suggest 21.5-22.5 million

terminals.

Short description of the market situation. At

the beginning of the year, the situation was promising on the Russian

terminals market. Although the market growth was detected, the growth

dynamics were slowed down by such inconveniences as the shipments

detention in the customhouse. The situation in the first quarter

is to be reviewed below along with its development.

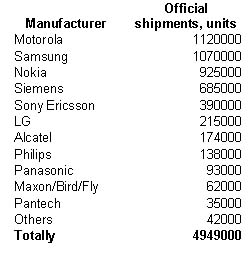

Official shipments of terminals suggested 5 million 107 thousand

in the first quarter. As compared to the previous quarter, the increase

of sales is 21 percent. However, the shortfall of equipment that

happened due to the shipments detention in the customhouse was still

a problem in March and February. Only at the end of March, distributors

started obtaining the cargos ordered previously. This process was

synchronized for all the companies and as a result, the problem

of stocks bigger, than the current companies’ needs, had to be faced.

The game of these stocks realization and price decrease had to be

began. The game of the price decrease started in the last week of

March and lasted during the second quarter.

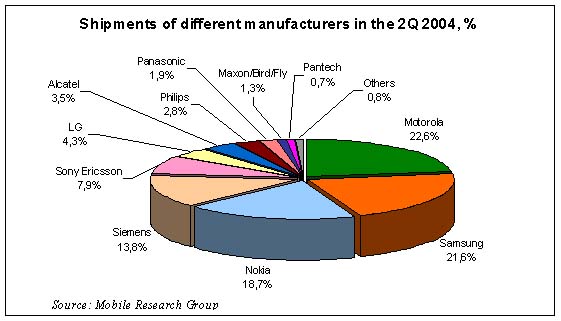

Market shares in the 2Q 2004

This process has negatively influenced the off-loading in the second

quarter (mainly in April and March) and some of the companies did

not manage to increase its shipments (Siemens, Nokia). This situation

encouraged the market share decrease of the LG Company that had

moved to the sixth place giving way to Sony Ericsson.

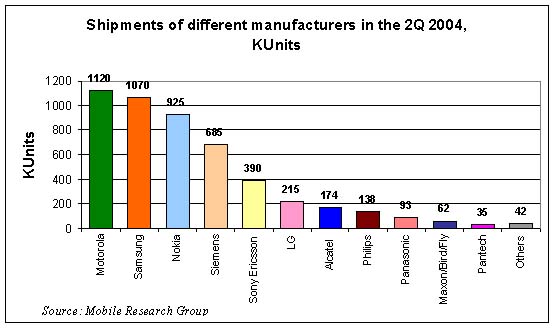

Shipments of the mobile terminals by model in the second quarter

2004 were the following:

The first four leading manufacturers remained the same; the overall

shipments decreased for every one of them. At the same time, the

gap between Samsung and Motorola diminished. This happened due to

the rejection at the beginning of the second quarter of already

place orders for Motorola phones by some of the distributors. On

the other hand, there were no such problems for the Samsung Company.

Although having rejected two low-end models (Samsung R210, N500)

that made a big share of overall sales, the company managed to compensate

their absence with the new models of the middle segment having increased

their supplies. The company has stabilized its position at the time

of lower market volume. Now it is the most favorable company of

all the distributors since the realization of Samsung phones is

outstanding and the margin is high.

As compared to the first quarter, the decrease of the market volume

diminished by three percent, which happened due to the low April

sales and the overstocking of the distribution channels.

The decrease of the average price as compared to the first quarter

is to be overlooked below. Such comparison may help to perceive

the situation and characterize it fully.

The decrease of the average selling price had a positive impact

on the Sony Ericsson production only; the company managed to increase

its market share mainly due to the shipments of inexpensive models

(T100, T105, and T230). At the same time, the supplies of the models

of high and middle price segments were preserved on the superior

level. Models such as T610, T630, and P900 were still in deficit.

The reduction of the average price was 19 percent for Nokia, which

is a very high indicator that stands for the demand of the inexpensive

models solemnly. Now, Nokia 3310 ranks for the highest sales although

it is fairly out of fashion. Among the models of the high price

segments, Nokia 6230 is the only one to be in a big demand. However,

the company did not manage to provide the shipments of this phone

in the sufficient amount. Several new products (Nokia 661I, N-Gage

QD) were taken rather coolly and their supplies were minimal. The

company is on the edge now - if there is to be no price default

by 15-20 percent, the company will start loosing its market share.

Currently, Nokia does not have a formed product range and models

capable of competing with other manufacturers when the price is

concerned. In the view of MRG, Nokia becomes associated with the

low-end phones, which certainly sheds a shadow on the name of the

brand. If the company does not change its strategy, it will end

up loosing from two to four percent of the market share during the

third and the fourth quarters.

Grey imports suggested 203000 terminals or four percent of the

total official shipments. As compared to the first quarter, the

decrease of the grey market shipments was one percent. Presently,

there are no grounds for the grey market growth.

The turbulences in the Communications Ministry in the second quarter

had a negative influence on the market of the mobile phones. Due

to the lack of the commission responsible for the licenses of the

new models, the manufacturers did not manage to certify the new

models that were supposed to enter the Russian market at the end

of the second and beginning of the third quarters. Consequently,

the companies had to overlook their plans of equipment supplies

to the Russian market and some of the manufacturers started the

shipments and the models’ advertising without certificates (that

is the violation of the Russian legislation). The situation had

mostly influenced Sharp Company that postponed its entrance on the

Russian market originally planned for the end of May-beginning of

June. The impact on other manufacturers was not that strong, although

it was still significant (view the MRG press-release №3, 4 for June).

Forecast for the 3Q 2004

The mobile phones certification will influence negatively the market

of the mobile terminals in the third quarter. The seasonal troubles

with the Russian customhouse (just like in the last year) are to

be expected. Thus, the market potential will not be realized to

its fullest. Consequently, there will not be any radical sales increase.

The rather pessimistic forecast of Mobile Research Group suggests

5 million 200 thousand terminals for the market.

About Mobile Research Group

The main activity of Mobile Research Group (http://www.mobile-analytics.ru)

- is mobile terminals market researches in Russia. The company

analyses the competitive situation of all mobile phones manufacturers

available on the Russian market, and researches retail and

wholesales of mobile terminals. Basing on analyzed statistic

data the company makes a forecast of the mobile terminals

market development for some period (up to one year). According

to concluded partnership agreement once a quarter the company

presents a market analysis report, where the most considerable

events and their results are marked.

Publishing data contained in this press release

without a link to the Mobile Research Group as a source of

information is prohibited. We reserve the right to change

data published above if any new circumstances or new information

earlier unknown to us arise.

© Mobile Research Group, 2004

Eldar Murtazin (eldar@mobile-review.com)

Translated by Maria Kapustina (maria@mobile-review.com)

Published — 03 August 2004

Have something to add?! Write us... eldar@mobile-review.com

|