|

|

Russian market of mobile terminals in the 2Q 2005

Press release, August 2 2005

Statistics: Official shipments of GSM-terminals on the Russian market suggested

7144 thousand terminals, while in the first quarter of 2005 official shipments suggested 8 004 thousand terminals. The decrease of sales was

10.7 percent, and it is typically seasonal. The grey market shipments suggested

8 percent, this slight growth is caused by the deficiency of some popular models. The growing

replacement market suggested 61 percent by the quarterly results.

The value of shipments suggested

737 million 393 thousand Euros (only official shipments).

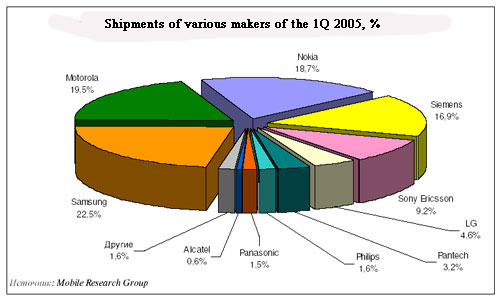

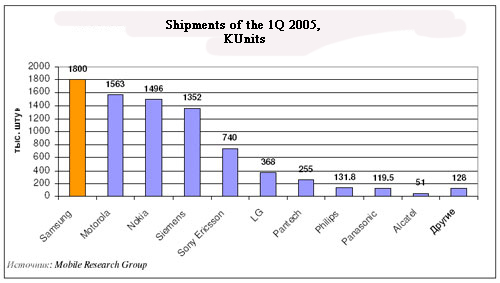

Short description of the market situation. Russian market suffered seasonal sales decrease in the 2Q of 2005. For better understanding of the situation let's review the manufacturers' positions in the 1Q.

The shipments arranged the following way:

In the 2Q the general supply formed 7 million 144 thousand 800 terminals,

which is 10,7 percent reduced as compared to the 1Q. The decrease is seasonal and typical for the Russian market. The grey

market grew 8.7 percent , which was caused by the troubles with the Russian customs,

high demand of models poorly shipped to the Russian market. The general market volume with the grey one

included formed 7 million 772 thousand 100 devices. The grown replacement market forms 61

percent by the quarterly results. The value of shipments suggested 737 million 393 thousand Euros (only official shipments).

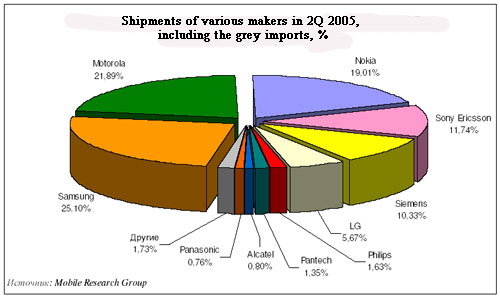

The 2Q market is characterized by high indicators of the replacement market, which caused demand for balanced models of the middle segment and expensive phones. With the preserved demand for low-end models, some displacement to the best in price/quality ratio models by various manufacturers was observed. The lack of such models resulted in deficiency for some makers, which provoked the 3 percent growth of the grey market. The ASP of the grey market considerably grew in the 2Q.

In the course of the quarter the minimal demand from the distributors' side was observed in May, and April sales were moderate. Wholesale channels' overstocking is considered a reason, it happened in the end of the 1Q when manufacturers tried to ship as many terminals to the Russian market as possible. As a result, the market has got livelier since the beginning of June, and the growth will go on in the third quarter.

The Russian Customs caused the main problem of the 2Q. Ground channels have finished normal functioning since May, the custom clearance got twice more expensive (from 3-4 Euros to 6-13 Euros, unofficial tariffs). In the end of May troubles with over the air shipment started, which caused deficiency in some positions. This influenced the market negatively, but on the other hand, preserved the prices on the same level, no seasonal price decrease for the current type products happened.

The company of Samsung fixed its sales on the level of the previous quarter. The indicator is positive under the condition of less marker value, but the company has changed its strategy as well. Some artificial deficiency had been supported till the 2Q, which caused high margin for distributors. In the 2Q, on the contrary, the company liquidated the deficiency and shipped the demanded value of terminals. No artificial limitations were put. The result was the May sales and margin fall for Samsung phones. The situation improved in June, we observed the margin growth for Samsung's devices. We can consider this as experiments with the market flexibility for the certain brand. Taking into account the deficiency was liquidated in the 2Q, it all told upon other manufacturers in the low market, and Nokia being the primary.

Nokia showed the record product line in the 2Q, which formed 40 models. At that 20 models were niche and assortment with the minimal sale indicator. The Samsung's actions influenced Nokia negatively and caused moderate sales. Nokia has stable sales of budgetary phones, at the same time fashion products have short life cycle and aren't sold widely. This prevents the company's market share from growing, but on the other hand forms a positive company image in the eyes of the customers, who consider a phone a good mean for investment and react negatively on fast price fall. Nokia competes with Samsung, Motorola and Siemens's low-end solutions. It's hard to increase the sales at a high model price, which tells upon its position.Traditional distributors of this manufacturer reduced purchase typically, and the company of Euroset has become the biggest by the quarterly result (both among retail and wholesale companies).

The company of Motorola can't provide with a firmed model line, the product line is weak. At the same time, they have some unique models, which are actively used for the promotion of the line. Thus, the Motorola RAZR V3 is lacking, this thin metallic clamshell has become one of the most popular in its price segment. Unofficial shipments grew, and retail prices fixed due to the absence of enough models. Besides Motorola RAZR, the company aggressively promoted Motorola E398, which is the cheapest memory-card-equipped device. This model is also in deficiency. The company could increase the ASP due to the grown sales of mid-level and high-end phones. Also they managed to fix the prices on the level of the 1Q.

The company of Sony Ericsson keeps on increasing its market share aggressively. Low-end company models are not very popular in retail and among distributors due to non-profitable price/quality ratio. At the same time such mid-level models as Sony Ericsson T630, K500 and K700 had highest sales in their segments, which allowed the company to increase its market share. Still Sony Ericsson K750 is the leading headset, though official shipments were minimal in the 2Q. The market volume of the model was the maximum, and the deficiency of the official shipments caused the growth of the grey market, which was the highest one. The model has no rivals, and the company decreases its price to prolong the life circle. We think Sony Ericsson K750 won't have real competitors till the middle of the 1Q 2006. And taking the fall of the model price into account, we can suggest it'll be shipped in significant amounts till 2006. The company has positive perspectives on the Russian market; its products are of high demand among end-users and distributors.

The fewest terminals by Siemens were shipped in the 2Q, which was caused by the 1Q overstocking. The sales volume was influenced negatively by seasonal decrease of the demand and the lack of new models. Siemens has lost the market, and the announcement of the mobile department given to BenQ negatively influenced the customer loyalty to the brand, and the main consequences will be to the fore in the 1Q 2006. In the 2Q the company took a passive position not shipping more terminals to the market and thus making an artificial deficiency. Distributors managed to normalize the sales volume for the Siemens brand and assess the demand for its terminals. As a result, we can't expect the sales growth for this brand; the company might increase the shipments, but still will lose to Sony Ericsson in this factor.

The company of LG generated a new strategy for the Russian market. They launch new models fast besides aggressive advertising. Due to this, they managed to increase the 2Q shipments, which caused positive growth. The after-sales service problem is almost solved, and no pressure from the side of end-users is suffered. The perspectives of this fact are better maker's image and trust in its products. At the same time the hardware platform of the current models is outdated and put some serious constraints (organizer for 20 entries, phonebook restrictions). The speed of new model launch will play the most important role, as well as getting rid of rudimentary functions. The company perspectives on the Russian market seem positive, they promise a 10 percent market share by the end of 2006 with the same aggressive advertising kept on.

The company of Pantech suffered several problems in the 2Q, which were concerned with wholesale channels overstocking in the 1Q, and low product sales in April. This induced the company to decrease the prices of the whole model line in the end of May; the price decrease was the maximum and formed 5-30 percent for some models. This, however, has an insignificant influence on the warehouse stocks. The main disadvantage is the activeness of the main national networks on regional markets, the washout of the Pantech products, and some unwillingness to work with the brand due to the lacking after-sales service. Pantech decided on establishing a special sub-company for after-sales service of this brand phones. Though the solution doesn't seem logical, since present service centers have all the necessary elements and only need necessary information and equipment, and manufacturer's control. The company will manage increasing its shipments in the 3Q, but the share growth will still be insignificant.

The second echelon companies suffered problems with selling terminals in the 2Q. Such companies as Philips have fixed their sales rate, which was due to the active promotion of Philips 650 from the Xenium line. The company stressed this device provides with the longest battery life in the standby mode. The Philips ASP grew due to the growing sales of the one model, and they formed the level of the 1Q.

Sagem and Alcatel look unsuccessful against this background, they are becoming niche on the Russian market. After a successful 1Q Panasonic faced the sharp sales fall, which was caused by slight price decrease for the current line, the lack of new models, overstocking of the wholesale channels. The company's perspectives are negative, fast model line renewal or the price policy change is necessary.

As a third echelon player, the company of Voxtel showed positive tendencies. They used the Svyaznoy network for distributing their models, which allowed increasing the shipments to the Russian market and keep high ASP. The 9th place on the Russian market may belong to Voxtel in 2005, that means displacing Alcatel in the sales volume.

The company of Sharp managed to deliver several thousand terminals to the market; it has become a niche player influencing the market in no way. The same for NEC, but the growth of i-mode terminals for the MTS network will be observed. This will allow the company to become a 3rd echelon player with a notable sales volume.

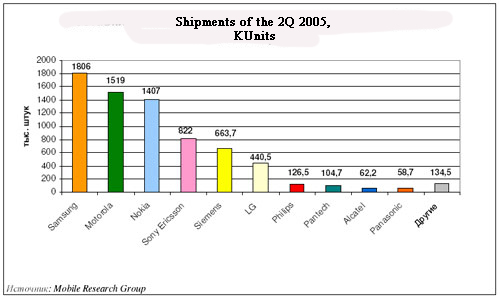

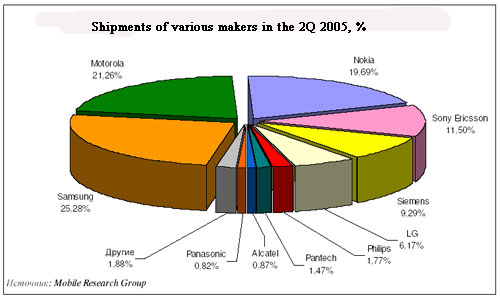

The sales structure of the 2Q looked this way:

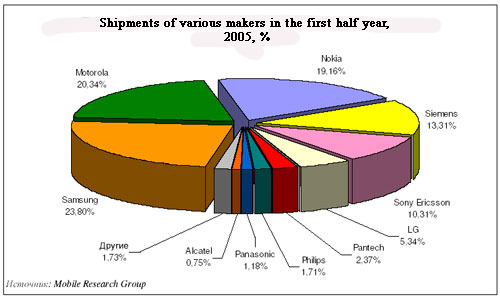

The results of the first half year on the Russian market

According to the two first quarters the companies are positioned this way:

1.Samsung

2. Motorola

3. Nokia

4. Siemens

5. Sony Ericsson

6. LG

7. Pantech

8. Philips

9. Panasonic

10. Alcatel

11. Others

The first three companies will most likely remain the same. As for the second half year results, the company of Sony Ericsson may displace Siemens from the fourth position. As for now, the makers' shares look this way:

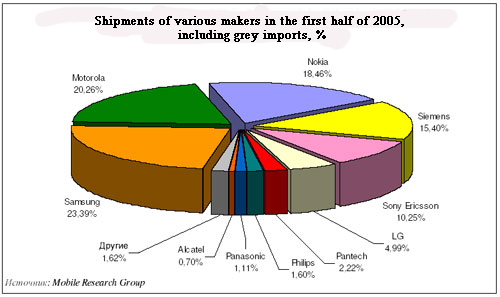

And here is how they look taking the grey market into account:

All the companies showed the change of their ASP in the 2Q, except for Motorola with its successful sales of the RAZR V3 and Motorola E398. Philips 650 was the best sold model for Philips. And the growth of the Pantech's ASP was caused by the double fall of the sales.

About Mobile Research Group

The main activity of Mobile Research Group (http://www.mobile-analytics.ru) - is mobile terminals market researches in Russia. The company analyses the competitive situation of all mobile phones manufacturers available on the Russian market, and researches retail and wholesales of mobile terminals. Basing on analyzed statistic data the company makes a forecast of the mobile terminals market development for some period (up to one year). According to concluded partnership agreement once a quarter the company presents a market analysis report, where the most considerable events and their results are marked.

Publishing data contained in this press release

without a link to the Mobile Research Group as a source of

information is prohibited. We reserve the right to change

data published above if any new circumstances or new information

earlier unknown to us arise.

© Mobile Research Group, 2005 Eldar Murtazin (eldar@mobile-review.com)

Translated by Maria Mitina (maria.mitina@mobile-review.com)

Published - 8 August 2005

Have something to add?! Write us... eldar@mobile-review.com

|

News:

[ 31-07 16:21 ]Sir Jony Ive: Apple Isn't In It For The Money

[ 31-07 13:34 ]Video: Nokia Designer Interviews

[ 31-07 13:10 ]RIM To Layoff 3,000 More Employees

[ 30-07 20:59 ]Video: iPhone 5 Housing Shown Off

[ 30-07 19:12 ]Android Fortunes Decline In U.S.

[ 25-07 16:18 ]Why Apple Is Suing Samsung?

[ 25-07 15:53 ]A Few Choice Quotes About Apple ... By Samsung

[ 23-07 20:25 ]Russian iOS Hacker Calls It A Day

[ 23-07 17:40 ]Video: It's Still Not Out, But Galaxy Note 10.1 Gets An Ad

[ 19-07 19:10 ]Another Loss For Nokia: $1 Billion Down In Q2

[ 19-07 17:22 ]British Judge Orders Apple To Run Ads Saying Samsung Did Not Copy Them

[ 19-07 16:57 ]iPhone 5 To Feature Nano-SIM Cards

[ 18-07 14:20 ]What The iPad Could Have Looked Like ...

[ 18-07 13:25 ]App Store Hack Is Still Going Strong Despite Apple's Best Efforts

[ 13-07 12:34 ]Infographic: The (Hypothetical) Sale Of RIM

[ 13-07 11:10 ]Video: iPhone Hacker Makes In-App Purchases Free

[ 12-07 19:50 ]iPhone 5 Images Leak Again

[ 12-07 17:51 ]Android Takes 50%+ Of U.S. And Europe

[ 11-07 16:02 ]Apple Involved In 60% Of Patent Suits

[ 11-07 13:14 ]Video: Kindle Fire Gets A Jelly Bean

Subscribe

|